In our last post, Outlook for the 2020s, I outlined the big picture for the coming decade as I see it. I argued on valuation grounds that both nonUS stocks and physical commodities will outperform US stocks. Moreover, while US Treasuries are more attractive than most other sovereign bonds, especially European and Japanese sovereign bonds, they should not be expected to turn in anything like the stellar performance of the first twenty years of this millennium. But what does that mean in terms of portfolio construction? Is it a good idea, for example, to avoid US Treasuries?

No. A good investment portfolio is more than just a collection of good investments. How they work together determines the level of risk involved. Even if US Treasuries turn out to be the mediocre performers I anticipate, they nevertheless are still likely to have a low to negative correlation with stocks. So a portfolio that includes stocks is likely to be less volatile if it also includes Treasuries than if it does not. This in turn means that if you have to tap your portfolio at some point, you’re less likely to be forced to sell an asset that’s in the dumper than if everything in it tends to rise and fall together. For the same reason, gold is an excellent asset to include in a portfolio with stocks, even when it doesn’t sport especially high returns itself.

As it turns out, of the physical commodities I track – copper, gold, silver and platinum – gold probably has the least upside potential over the coming decade. It looks better than US stocks, and due to its low correlation with stocks, should be part of every investment portfolio. But over the coming years, I nevertheless expect silver to outperform gold. As of the beginning of this decade, copper is a bit cheaper yet, and therefore has more room to mean revert to the upside. Finally, of these four physical commodities, platinum is historically the cheapest, and consequently has the most room to rise.

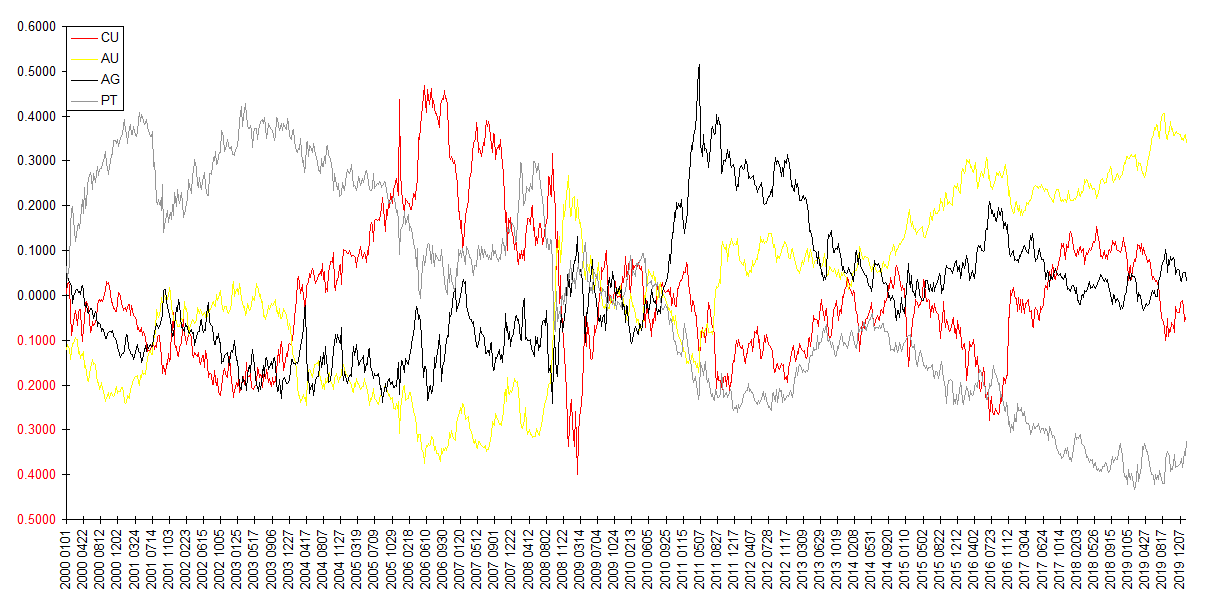

But since none of these commodities has a cash flow, what can we use as a basis for valuation? This is based on an analysis of their current prices relative to their historical ratios over the first two decades of the 2000s. The below chart gives a visual indication of this. Specifically, it is of the log prices of each since the beginning of 2000, normalized to their mean levels, and plotted relative to the mean of the four. The result indicates how the price of each has fared relative to the group, and eliminates the dollar from the picture.

As you can see, the chart indicates that the last decade ended with, and this decade opened with, gold as the most richly valued of the four, with platinum as the least richly valued of the four.

Bear in mind however that of the four commodities, gold is also the least correlated with stocks, so in a portfolio that includes a significant weighting in stocks, gold continues to merit a significant weighting as well. And its status as the most richly valued of the four commodities doesn’t mean it’s richly valued compared to US stocks; to the contrary it still looks cheap in comparison to US stocks.

What about other commodities? In reply to JK’s question about oil in my last post, I pointed out that oil is highly correlated with copper. The same applies to some degree to virtually every physical commodity, since we price them all in the same currency. While week to week correlations may be merely significant, over longer time frames this common denominator has typically been the overwhelming factor in commodity prices. Over the past several decades, for instance, most physical commodity prices have risen in dollar terms by about an order of magnitude, if only because the value of the dollar has fallen by about an order of magnitude. Given recent trends in US monetary and fiscal policy, and the likelihood for more in response to a deflating financial asset bubble and political attitudes towards debt and spending, this phenomenon should be obvious in spades over the coming years.

i’m skeptical that ev’s will get a big market share for many years, but isn’t the prospect of lower demand for catalytic converters weighing on platinum? if so, that would change the historical relationships of pricing among the metals.

It would. But platinum isn’t that heavily used in catalytic converters these days. Mostly in diesel, where it’s more efficient at the higher temperatures involved. In gasoline powered vehicles, palladium predominates. But palladium has risen in price to the point where designers are under pressure to consider alternatives such as platinum. Thus the surge in palladium prices in recent years itself is poised to become a driver of platinum prices. This process is likely to take time to play out, as regulatory approval is required for new emissions control designs, but since the time frame under consideration is a decade, that’s just the kind of ‘catalyst’ we’re looking for.

Moreover, much of the catalyst content in converters is reclaimed and recycled, so net consumption is far less than initial use … unlike oil, the metal itself isn’t burned up.

On the other hand, the basing pattern in the chart could be an early sign markets are beginning to factor in platinum’s potential. Platinum prices have turned sharply higher in recent months, even on a relative basis.

Meanwhile the price relationships at work predate specific industrial applications. Platinum has other important industrial applications besides catalytic converters and is a monetary commodity as well, being used for the US platinum Eagle and the Isle of Man coins for example. It’s also used in jewelry. Platinum is rarer than gold and has a long history of pricing above that of gold on an ounce for ounce basis. A platinum record is a higher award than a gold record. With current gold prices above $1500 per ounce, platinum at around $1000 is a historic bargain.

Finally, my remarks about platinum in particular are subordinate to the broader point about the commodity price outlook. Even if I were wrong about the relative relationship of these particular commodities it would be hard to go wrong with any of them. As a practical matter a 2020s commodity allocation would ideally diversify among them; in dollar terms the primary price driver will be money printing and inflation. My analysis regarding platinum wouldn’t be a suggestion to focus on platinum to the exclusion of others, but rather not to omit it.

As it turns out there was just news on a breakthrough in catalytic converter technology that allows platinum to be partially substituted for palladium:

https://www.msn.com/en-za/money/markets/pgm-game-changer-basf-sibanye-and-implats-unveil-new-tri-metal-gasoline-catalyst/ar-BB110zB5

chart of xle.spx shows full circle, low in 1999, high in 2008, back to its lows now. just a coincidence i guess.

https://twitter.com/HFI_Research/status/1219842628289609728

Not sure what your point is, but SPY and XLE are both stock funds.

the point is that xle, equity in energy companies, is extraordinarily undervalued relative to the general market. i.e. another data point supporting your thesis.